Introduction

One of my sons is a newly minted accountant. He dreams of someday managing a hedge fund. We spend hours talking about modeling data and making predictions. These discussions have convinced me that I need to know more about financial engineering. To learn more about the subject, I have been watching Youtube videos by the Bionic Turtle. I enjoy these videos because they are informative and short (my attention span is not what it used to be, and it wasn't good even then).

Anyway, the other day I watched a video by the Bionic Turtle on leasing automobiles. Normally, computing lease payments requires using time value of money equations. During the Bionic Turtle lecture, I found that the automobile dealers use an approximation to the time value of money equations that makes their calculations much simpler (i.e. they can be done on a "four banger" calculator). Unfortunately, the video did not go into any detail about the approximation. Since my entire career is a celebration of detail, I could not let this go. 🙂

Kidding aside, I found that deriving the approximation interesting and worth going through here. The derivation involves the creation of a term called the "money factor." Since I do not like "magic numbers" in calculations, I wanted to know where this term comes from.

Note that I do not lease my vehicles. I buy them and drive them into oblivion. My interests here are strictly mathematical. That said, let's dig in ...

Background

Approaches to Lease Modeling

The basic concept of auto leasing is simple:

- You are using a depreciating asset.

- The auto dealer expects you to pay for the depreciation.

- The auto dealer expects to earn a competitive return on his investment.

- At the end of the lease period, you return the auto to the dealer. He can then sell or lease the used vehicle to someone. Of course, you can decide to buy the vehicle at the end of the lease period.

We can look at the problem from three points of view: future value, present value, and money factor approximation. Fortunately, the future value and present value solutions provide us exactly the same answer. The money factor approximation is useful in that it allows a very accurate loan payment approximation to be computed without having to take numbers to powers. I will go through the math for each point of view.

Pricing

Price is a complex thing when it comes to leasing. For the purposes of this post, I will use four forms of price:

- PL is the list price.

Almost no one who buys a car pays list price. Nearly everyone negotiates the price down even a little. I personally have negotiated car prices at "no negotiation" dealers. This is important especially for new car owners who need to ship their cars using a shipping service similar to CarsRelo. The main use of the list price in my analysis here is in determining the value of the car at the end of the leasing period. This is often done as a percentage of the list price. - PN is the negotiated price of the car.

This is the price agreed upon by the lessor and lessee. - PF is the amount of money being financed through the lease.

People who lease cars often have to make a down payment, which reduces the amount of money that is covered by the lease. - R is the residual value of the car at the end of the lease. It is often expressed as a percentage of the list price.

Interest Rates

I express the lease interest rate in two equivalent forms:

- I is the lease's annual percentage interest rate.

- i is the per payment interest rate.

Since most leases assume monthly payments,.

Analysis

In the following analysis, I will be working through a lease example from this web site. I liked their approach and thought it was a good example. My focus is on explaining the use of an approximation in determining the value of the lease payment.

Future Value Viewpoint

Figure 1 summarizes the derivation of the lease from the future value standpoint. It includes a worked example that shows how to handle the case of making a down payment and negotiating a lower price. As stated earlier, the example is from here. Note that I model the lease payments as an annuity due (information here).

Figure 1: Derivation of Lease Payment Formula From Future Value Standpoint.

Appendix A shows the same calculation performed using Excel. The results are identical.

Present Value Viewpoint

Figure 2 shows how the same lease payment formula can be derived from the present value viewpoint.

Figure 2: Derivation of Lease Payment Formula From Present Value Standpoint.

Money Factor Viewpoint

This analysis is interesting to me because of its focus on dealing with averages. Here is a summary of the approach.

- Cars are a depreciating asset. The person leasing the car must pay the depreciation.

- The total interest paid on the lease is equal to the total payments made minus the amount financed (PF).

- The amount of the payment is equal to the average interest paid per payment plus the average depreciation paid per payment.

We can summarize the last bullet with Equation 1.

| Eq. 1 |  |

where

- P is the monthly lease payment

- PI is the average interest paid per lease payment

- PD is the average amount of depreciation paid off per lease payment

We can calculate the average depreciation paid per payment as shown in Equation 2.

| Eq. 2 |  |

Determining the average interest paid per payment is a bit more complicated. The keys to determining this relationship are:

- Use of the Taylor series substitution

.

- This means that

.

Equation 3 summarizes the derivation.

| Eq. 3 |  |

|

| After much painful algebra ... | ||

|

||

|

||

Assume that  , which means that , which means that  can be replaced by can be replaced by  with minimal error. with minimal error. |

||

|

||

|

||

|

||

|

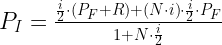

We can substitute Equations 2 and 3 into Equation 1 to obtain Equation 4, which is the equation the auto dealers use.

| Eq. 4 |  |

Figure 3 shows that we can work the example of Figure 1 without using powers of numbers and obtain nearly the same answer with much less mathematical effort.

Figure 3: Worked Example Using Money Factor.

The exact solution gives a payment value of $311.61 and the approximation gives $312.22. This is an error of 0.2%. Not too shabby.

Conclusion

In this post I looked at leasing from a classical viewpoint (present value and future value) and from an approximate viewpoint (money factor). I worked through an example that show that difference between the results is a fraction of a percent. This approximation makes sense for common use because it avoids the human calculator from needing to deal with powers of numbers, which for many folks is an issue.

Appendix A: Car Lease Payment Calculation in Excel

Figure 4 show the same calculation done using the Excel PMT function.

Figure 4: Lease Payment Calculation Using Excel.

Pingback: I Stumbled Upon Some Math Today… | PTC

I just started looking at leasing a car, and I derived from the equation for the "money factor" that the car lease calculators were effectively charging interest on the average of the initial price & the residual price. I suspected that this was close to the amount of interest computed with the exact loan formula, but I didn't realize it was so close! My mind is now at ease from seeing your rigorous derivation. Thanks!

As far as I am concerned, everything associated with car dealers is suspect until properly verified. Also, I do not like "magic formulas." Whenever I encounter them, I have to try to figure them out.

Glad the post was of use.

Mathscinotes

As a sales manager at a car dealership I can understand your concern. As in any kind of sales there can be a lot of tricks to be worried about. In our case we are a small family owned dealer and we CAN sleep at night. In any case I have a question regarding your lease calculations above. I created a Microsoft Access Lease database that incorporates a money factor for calculating leases. It works extremely well and allows our salespeople to quickly and easily figure lease payments for any of the vehicles we sell without having to look up individual money factors or residuals for each vehicle they want to lease. The one thing I have not been able to work into the formula is how to include credit insurance. We don't push credit insurance on anyone, but occasionally someone will demand it, and I would like to be able to incorporate it into the program. Is this something you know anything about?

Regarding your (1) Future Value Viewpoint and (2) Present Value Viewpoint--

There are notational inconsistencies.

And there are errors in the results because your monthly payment formulas don't take into account the fact that lease payments occur at the start of each period rather than the end of the period.

These are the corrected formulas:

(1) Future Value Viewpoint:

FV = Pf * (1+i)**n

FV = P(1+i)[(1+i)**n - 1]/i + R where P = monthly payment.

Solving for P:

Pf * (1+i)**n = P(1+i)[(1+i)**n - 1]/i + R

Pf * (1+i)**n - R = P(1+i)[(1+i)**n - 1]/i

i * [Pf * (1+i)**n - R] = P(1+i)[(1+i)**n - 1]

P = i * [Pf * (1+i)**n - R] / {(i+1)*[(i+1)**n - 1]}

(2) Present Value Viewpoint:

PV = Pf

PV = P*(1+i)*[1 - (1+i)**(-n)]/i + R*(1+i)**(-n)

Solving for P:

Pf = P*(1+i)*[1 - (1+i)**(-n)]/i + R*(1+i)**(-n)

Pf - R*(1+i)**(-n) = P*(1+i)*[1 - (1+i)**(-n)]/i

i* [Pf - R*(1+i)**(-n)] = P*(1+i)*[1 - (1+i)**(-n)]

i* [Pf * (1+i)**n - R] = P*(1+i)*[(1+i)**n - 1]

P = i* [Pf * (1+i)**n - R] / {(1+i)*[(1+i)**n - 1]}

The computed payment is $311.608.

(I compute the same payment using MS Excel's PMT formula.)

You are correct. I have updated my Mathcad to reflect the annuity due calculation. I have also included an Excel example. Many thanks!!

mathscinotes

Terrific article. Were Brach's corrections reflected in your webpage, above? If not, can I get a copy of the corrected work? I find Brach's notation difficult. Thanks! (I always wondered about the "24" too.)

Article is up-to-date.

mathscinotes

Pingback: Auto Insurance Buy Vs Lease Analysis Excel | autoksk

Pingback: Auto Car Buy Buy Vs Lease Analysis Excel | autoksk

Dear Mark,

I found your note while trying to answer the same question as you did (... 8 years ago it seems!). My computations are similar to yours, but - thanks to you(!) - my conclusion is a bit different. If I dare, here are my thoughts.

First, the references that I am following seems to favour what I am guessing was in the first version of this note, namely that

(*) PF*(1+i)^N = P*[(1+i)^N - 1]/i + R

(I am using the notations that you introduce in your "Future Value Calculation" frame in for example "eq1", indeed, as Brach notes, they seem to change, in particular in the "Money Factor Viewpoint")

The idea for the right-hand side of the equation is that at the beginning of the contract, you make a first downpayment D (participating, as you write, in making PN into PF) and at the beginning of _next_ period, you start making the regular monthly payments. This point of view comes from on-line documents for courses given either in France or Switzerland, so conventions might be different in other countries.

Second, your computations (starting with Eq.1) seem to use the formula (*), and I will also use it to estimate the lease monthly payment:

(**) P = (PN*(1+i)^N-R)*i/[(1+i)^N - 1]

-The first approximation (rather harmless - though it can be illegal in certain countries for financial transactions) is for the interest: i=I/12 is the average monthly interest instead of the monthly interest i=(1+I)^(1/12)-1. Indeed, compounded over 12 months, the latter yields the same interest as the yearly interest I. Or, if you prefer: i=I/12 is obtained by truncating the Taylor series of i=(1+I)^(1/12)-1.)

-The second approximation, is made, as you mention, by using the Taylor series: replace (1+i)^N by its Taylor expansion (1+N*i+T) up to any term you want, where T stands for the remaining terms. Replacing this in (**) yields

P = [PN*(1+N*i+T)-R]*i/(N*i+T)

= (PN-R)*i/(N*i+T) + PN*(N*i+T)*i/(N*i+T)

= (PN-R)*i/(N*i+T) + PN*i

-Third approximation: truncate the Taylor series (N*i+T) to N*i, so that

P = (PN-R)/N + PN*i

-To get the formula dealers use, a fourth approximation is apparently made: replace PN*i by (PN+R)/2, to obtain

P = (PN-R)/N + (PN+R)*I/24

So, my question is "Why the fourth approximation?"; PN*i is easier to use than (PN+R)*i/2. All the other approximations are Taylor series truncations, but this approximation is mysterious for me. Some very brief simulations show that this formula yields small differences in monthly payments, so there is apparently no real problem for actual transactions (and for some of these approximations, the client gets off better than the dealer by a few cents or dollars). But my interrogation remains... And any answer is welcome!

Cheers,

Gavin

Dear Mark,

Thanks for your interesting derivation of Dealer's formula for monthly payment amount for auto lease. I tried myself to derive the same formula from the exact formula using some approximations. It seems like that the key steps in the derivation may be reduced to the following two useful approximations . i.e.

1) (1+x/N)^N =e^x (1+O(x^2/N)) for large N ( Euler's formula for e^x )

2) e^x =(1+x/2)/(1-x/2) +O(x^3) for small x ( Pade Approximation for e^x )

where x=I*N/12.

Thanks again for your most interesting article.

Histo